By Maha Farooq – Equity Analyst

Herbalife Ltd

Ticker HLF (NYSE)

Based on Q3 Earnings release

Investment thesis

Herbalife (HLF) is showing early signs of operational recovery driven by North American segment returning back to growth, debt reduction, disciplined cost control, digital platform expansion as well as improving distributor engagement. While margins remain pressured by inflation, the company’s transformation programs as well as deleveraging trajectory create a path towards its fair value of $34 per share based on our free cash flow valuation.

Overview

Herbalife delivered a strong Q3,2025 earnings results exceeding guidance on net sales as well as adjusted EBITDA. Notably the company achieved its first quarter of North Americans sale growth since 2021 suggesting significant turnaround. Additionally, Herbalife demonstrated material progress in financial discipline, evidenced by robust operating cash flow and reduced leverage. With strategic initiatives including the rollout of the Pro2col digital ecosystem, new product innovation like HL/Skin as well as extensive distributor training engagement the company is building a clearer pathway towards sustainable growth.

Financial overview

The company’s net sales for the third quarter 2025 reached $1.27 billion from $1.24 billion last year with a rise of 2.7% Y-o-Y. HLF’s revenue expanded by 3.2% with the most encouraging development being the long-awaited return of North America’s growth for the first time since 2021.

North America’s sale increased by 1% which is supported by 17% surge in new distributors indicating renewed engagement as well as an early sign that distributors productivity initiatives are taking effect. Whereas, Latin and EMEA delivered solid growth and Asia Pacific grew modestly. However, China remained a drag with a 4.7% decline due to the company mainly shifting its strategy towards gaining more preferred customers who purchase products directly from the company at a discount or loyalty price but are not involved in recruiting or selling like distributors. This led to a decline in sales which impacted sales volume. Profitability for the quarter reflected ongoing margin pressure as well as progress.

The company generated $43.2 million in net income and $51.5 million in adjusted net income compared to $42.8 million in Q3 2024. EBITDA reached approximately $12 million even after negative impact of foreign exchange headwinds. Gross margin in Q3 2025 was 77.7% slightly lower compared to 78.3% in 2024, due to currency impact, inventory adjustment and input cost inflation. Despite these impacts operating cash flow remained robust with Herbalife producing $138.8 million in Q3 2025 compared to $127.2 million in Q3 2024.

HLF’S strong cash generation enabled the company to fully repay the remaining $147.3 million of its senior notes in 2025. This helped the company reduce leverage to 2.8x from 3.3x , an improvement that strengthens the balance sheet by enhancing equity value potential as well as reducing refinancing risk.

The company’s strategic initiatives continued gaining traction. Distributor’s engagement significantly increased through global training events. While the company introduced HL/Skin a south Korean science driven skincare line supported by clinical studies as well as an AI powered facial analysis tool demonstrating the company’s focus on entering higher margin product categories that appeal to younger consumers.

The most significant long-term catalyst remains the rollout of Pro2col, the company’s coaching and digital health ecosystem expanded beta access to retail consumer in Canada, USA and Puerto Rico. The introduction of new features such as a coach dashboard, integrated website builder and customizable sales funnels with over 7,900 distributors are now using the platform and a broader commercial release plan by the end of 2025.

Source: Moods Investment Research

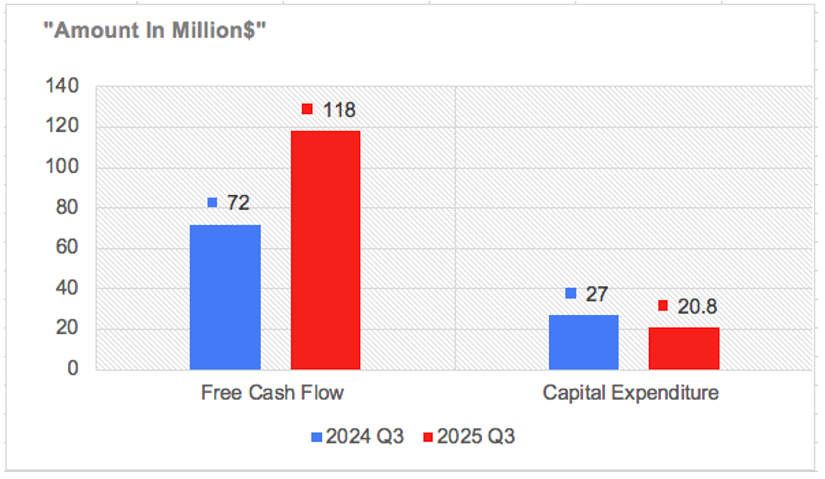

The company’s free cash flow strengthened significantly reaching to $118 million in Q3 2025 compared to the last year which was $72 million indicating stronger operating cash flow. Whereas, Capital Expenditure decreased to $20.8 million in Q3 2025 from $27 million in 2024 supporting the strong free cash flow performance.

DFCF Valuation

Fair Value Estimate

Based on Herbalife last 10 year’s free cash flow, growing at 3% and discounted at a conservative 12% we get a fair value of $34.2 per share, the valuation suggests significant upside of 300% in 3-4 years once fundamentals stabilize.

Other key metrics driving Herbalife towards its fair value.

| Metrics | 2025 (TTM) | 2024 |

| Debt-to-Equity | -3.62 | -3.08 |

| Debt-to-Assets | 0.82 | 0.91 |

| Debt-to-EBIT | 4.83 | 6.37 |

| Interest Coverage Ratio | 1.78 | 2.15 |

| ROE % | -52.45 | -26.53 |

| ROIC % | 20.88 | 16.22 |

| ROA% | 11.88 | 9.18 |

| P/E | 3.78 | 2.68 |

Herbalife’s financial metrics indicate mix performance trend between 2024 and 2025(TTM). Debt-to-Equity ratio of negative 3.62 in 2025 slightly worse than negative 3.08 in 2024 showing the company has more liabilities than equity indicating high financial leverage and risk. Debt-to-Assets has improved slightly from 0.91 in 2024 to 0.82 in 2025(TTM) indicating reduction and reliance on debt financing relative to company’s total assets. Debt-to-EBIT ratio declined from 6.37 in 2024 to 4.83 in 2025(TTM) showing the company’s efforts to cover its debt through its earnings. Although the company’s interest coverage ratio has decreased from 2.15 in 2024 to 1.78 in 2025(TTM) indicating a reduced buffer for meeting interest obligations.

Return on Equity remains negative at negative 52.45% compared to 26.53% in 2024 signaling losses relative to shareholders equity while Return on Assets has improved from 9.18% in 2024 to 11.88% in 2025(TTM) indicating Herbalife is generating higher returns from its assets despite poor equity performance. However, its ROIC has significantly increased from 16.22% in 2024 to 20.88% in 2025(TTM) showing improved efficiency in generating returns on the capital invested. P/E also rose from 3.68 in 2024 to 3.78 in 2025(TTM) that reflects market optimism about future earnings despite current challenges with profitability.

Overall the company appears to be improving operational efficiency as well as asset returns. However, the company still faces significant equity related losses.

Conclusion

Herbalife’s Q3 results indicate a meaningful turning point for the company after many years of poor performance. With the exceeding net sales as well as return to growth in the North America’s segment, substantial debt reduction and disciplined cost control, Herbalife has begun to rebuild financial strength and operating momentum. Strong operating and free cash flow coupled with improving balance sheet enabling the company to reinvest in product innovation, digital expansion as well as distributor’s engagement. While FX headwinds and macro factors remain, the company’s improving fundamentals and ongoing strategic initiatives position it well for sustained recovery as well as gradual move towards its fair value of $34 per share.

Disclaimer

The information provided by Moods Investment Research is for general informational and educational purposes only. It is not intended as, and does not constitute, financial, investment, tax, legal, or other advice. The content is not a solicitation or recommendation to buy, sell, or hold any securities or investment strategies.

All opinions expressed are based on current analysis and are subject to change without notice. While we strive for accuracy, Moods Investment Research

makes no representation or warranty as to the completeness, accuracy, or reliability of any information provided. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Moods Investment Research and its founders, directors, or affiliates are not liable for any losses or damages arising from any reliance on the information provided.

The views expressed in this article are those of the author(s) and do not constitute investment advice. The author does not hold a position in Herbalife. However, the author(s), including any editors or contributors (collectively referred to as “Moods and directors”), may or may not hold positions in other securities mentioned. Any such holdings are subject to change without notice.

Artificial intelligence (AI) technologies were used to support data processing, drafting, and/or analysis in this report. All conclusions and recommendations reflect the author’s independent judgment. While care has been taken to verify all information, neither the AI tools nor the authors guarantee accuracy or completeness. Therefore, whilst results derived from AI were reviewed for reliability; however, users should independently verify critical information.