Equity Analyst- Maha Farooq

May 17, 2026

Investment Thesis

Stride (LRN) Inc. represent a compelling long-term investment opportunity built on a structural shift in how education is delivered as demand for outcome-driven learning grows.

The company sits at the center of this transformation, operating a scalable, technology first platform across k-12 as well as career learning that serves over three million students.

Financially the company has demonstrated meaningful operating leverage, with net income and FCF growing faster indicating a scalable business model and discipline cost structure.

Despite these strengths the company’s valuation appears disconnected from its fundamentals. From a valuation perspective the company appears significantly undervalued based on a DFCF model, with an intrinsic value of $267 per share compared to current market price of $91 per share implying a substantial margin of safety. This valuation indicates the company is not fully pricing in its earnings power, long-term growth potential and operating leverage. Additional catalyst includes accelerating enrollment trends, continued expansion of higher margin career programs and a $500 million share buyback program that signals management’s confidence in intrinsic value.

Company Overview & Business Model

Stride Inc is a U.S based education technology provider that delivers online learning solutions through a comprehensive digital platform serving schools, organizations as well as students. The company supports the full education process, including enrollment, instruction, progress tracking and student support. Moreover, it also serves public as well as private schools, charter boards, school districts, government agencies, employers and individual learners. LRN operates across K-12 as well as adult education markets mainly focusing on general education core academic subjects and career learning job focused skills in fields like healthcare, IT, and business.

The company was founded in 2000 it has expanded to serve millions of students through virtual schools and training programs across many states.

LRN business model is primarily based on a school-as-a-service approach where the company provides an integrated package of curriculum, instruction, technology and support services to institutions. The company generates revenue primarily through long-term contracts as well as typically lasting over five years, creating stable and recurring income. Additionally, the company also sells standalone products and services such as training programs and curriculum.

The business model mainly focuses on scalable digital education, meeting the growth demand for flexible learning options and career-oriented training, while partnering with multiple institutions as well as organizations to deliver customized education and workforce development solutions.

Segment breakdown

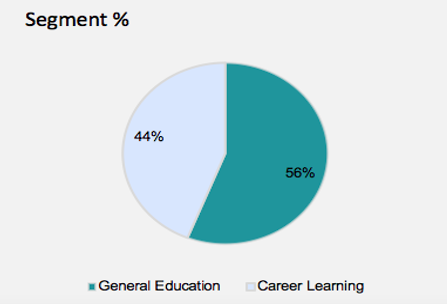

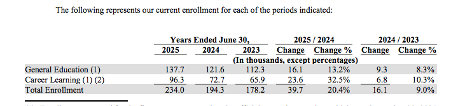

General Education: This segment focuses on core k-12 academic subject which is delivered through online school and services. This segment contributes the largest share of revenue. it generated a revenue of $1.34 billion as of 2025 contributing around 56% of total revenue driven by long-term contracts with public as well as private schools.

Source: Moods Investment Research

Career Learning: It includes career-focused programs for middle and high school students as well as adult training programs. Revenue generated from this segment alone was $1.07 billion as of 2025 accounting for about 44% of total revenue. While its segment is smaller than general education it is the faster growing segment, supported by increasing demand for job-ready skills as well as certification.

Financial Analysis (For the last 5 years)

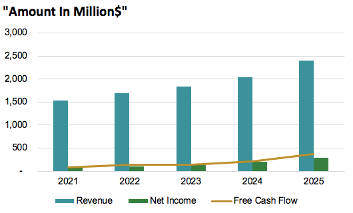

The company has shown strong and consistent revenue growth over the past five years, increasing from $1.54 billion in 2021 to $2.41 billion in 2025 representing a growth of more than 50% during this period. The company’s revenue grew steadily each year with moderate growth between 2021 and 2023, followed by a strong acceleration in 2024 of $2.04 billion and a significant jump in 2025 indicating increasing demand for online education particularly in career focused programs.

Stride Inc’s net income has grown has grown steadily from $71.5 million in 2021 to $287.9 million in 2025 indicating nearly 4x increase over the period. The company has shown great improvement between 2021 & 2023 followed by a strong acceleration between 2024 & 2025 indicating improving profitability, driven by higher revenue growth, operating leverage as business scales as well as better cost efficiency.

Source: Moods Investment Research

Free cash flow suggests a strong upward trend from $81.9 million in 2021 to $372.8 million in 2025 indicating significant improvement in cash generation. Solid growth between 2021 of $81.9 million and 2022 of $139 million. FCF increased sharply in 2024 and surged in 2025 indicating the company strengthened its ability to generate cash from operations, scaled its business effectively and improved efficiency which enhances its financial flexibility for debt repayment, investments or shareholders returns.

Source: Moods Investment Research

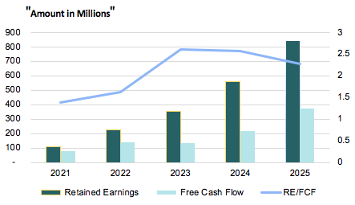

The company’s retained earnings grew strongly between 2021-2025 indicating that the company has been effectively reinvesting it earning, strengthening it financial position to support its long-term stability.

Debt Analysis

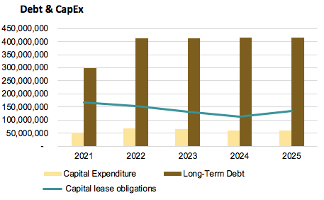

The company’s long-term debt indicated a noticeable shift over the last five-year period. debt increased significantly from $299 million in 2021 to $411 million in 2022 suggesting major financing decision to support expansion as well as strategic investments. However, after this peak the debt levels remained stable with only minor increase each year reaching to $416 million in 2025. This stability suggests that the company is not heavily dependent on borrowing and is maintaining a controlled approach to leverage.

Source: Moods Investment Research

The company’s capital lease obligations indicate a consistent declining trend for the last 5-years followed by a slight increase in 2025. The lease obligation decreased from $167 million in 2021 to $154 million in 2022, Moreover, it declined further to $130 million in 2023. This steady reduction suggest that the company was gradually repaying its lease liabilities and reducing its dependence on leased assets. However, in 2025 the lease obligations increased slightly to $133 million in 2025 suggesting that the company entered into new lease agreement likely to finance equipment such as computers and peripherals used in its operations.

Capex increased from $52.3 million in 2021 to $67.6 million in 2022 and remained relatively high at $66.5 million in 2023 and $61.6 million in 2024 and however, it declined to $60.0 million in 2025. Despite some fluctuations the trend indicates a gradual reduction in capital investment over time.

Competitor Analysis

| Metrics FY 2025 | Stride LRN | CVSA | LOPE |

| Market Cap | 6.3 B | 4.5 B | 4.52 B |

| P/E | 24.4 | 20.59 | 21.52 |

| ROE% | 21.68 | 16.92 | 28.24 |

| ROA% | 13.66 | 8.63 | 21.5 |

| ROIC% | 27.78 | 10.49 | 36.43 |

| Debt-to-equity | 0.37 | 0.54 | 0.14 |

| Debt-to-asset | 0.24 | 0.28 | 0.11 |

| EPS | 5.96 | 6.18 | 7.71 |

| FCF margin % | 15.5 | 16.08 | 21.57 |

The competitor analysis compares Stride (LRN) Adtalem Global Education (CVSA) & Grant Canyon Education (LOPE) across financial and performance metrics for year 2025. In terms of market cap all three companies are similar in size with Stride slightly ahead at $6.3B suggesting a marginally stronger market presence.

Stride has the highest P/E ratio of 24.4 followed by 21.52 of LOPE and 20.59 of CVSA. This indicates that investors might have higher growth expectations for stride while CVSA appears more conservatively valued.

Lope outperformed with highest ROE of 28.24%, ROA of 21.5% & ROIC of 36.43% suggesting superior efficiency in generating returns from equity as well as assets. Stride follows with solid profitability metrics ROE of 21.68%. & ROIC of 27.78% while CVSA lags behind in profitability ratios.

In terms of financial leverage LOPE is the least leverage company with the lowest debt-to-equity of 0.14 and debt-to-asset ratio of 0.11 indicating conservative capital structure, Whereas, CVSA has the highest leverage. Moreover, Stride maintains a moderate position.

EPS & FCF margin further highlight LOPE’s strong performance. Whereas, Stride and CVSA indicate relatively comparable FCF margins.

DFCF Based Valuation

The intrinsic value of the company was estimated using DFCF model based on the company’s FCF growth for the last 5 years. The company seems to be undervalued with a fair value of $267.05 per share assuming a discount rate of 12%.

When compare to its current price of $91 per share. Stride’s stock appears to be significantly undervalued indicating the market may not be fully reflecting its strong historical cash flow growth and future potential. Based on the DFCF valuation the stock offers a substantial margin of safety and represent an attractive investment opportunity.

Catalysts driving the company to its fair value

Key catalyst’s driving the company to its fair value primarily stem from its strong growth, strategic position in digital education and expanding market demand. One of the most important drivers is the continued shift towards online as well as hybrid learning, which led to rising student enrollment across its core K-12 and career learning segment.

Source: Company’s 10k Report

The rapid expansion of its career learning segment is focused on job ready skills like technology and healthcare has been a major catalyst with significant higher growth rate enhancing the company’s long-term profitability outlook.

Additionally, the company’s strong financial performance including double-digit revenue growth, rising operating income as well as robust free cash flow reinforce shareholder’s confidence and support valuation upside.

Stride Inc’s share buyback program is a very important catalyst, the company authorized a $500 million stock repurchaseprogram running through October 2026 suggesting strong confidence from management in the company’s fair value and future growth.

The company’s performance is a clear indicator that they are capturing significant market share the company’s stock climbed more than 350% since 2021. The growth and bold direction have delivered value to its shareholders and the more than 3 million families they served.

Several key risk that can impact the company’s performance

One of the major risks the company faces is regulatory uncertainty it operates in the educational sector where government policies, accreditation rules as well as funding can change and directly affect enrollments and revenue. The company also heavily depends on public perception of online education if students, parent and institutions lose confidence in virtual learning quality demand may decline. Furthermore, competition is another concern, from company’s like LOPE, traditional schools and universities.

Stride relies on enrollment growth so any decline in no of students due to demographic shifts or economic conditions could reduce the company’s growth.

Operational risk includes maintaining technology infrastructure, cybersecurity threats and ensuring consistent education quality across program.

Additionally, the company faces financial and legal pressures its increasing debt levels create a significant risk and reduces financial flexibility. If interest rates rise, borrowing cost will increase further, which will affect cash flows, reduce profitability as well as limit the company’s ability to invest in growth.

Moreover, the company currently is facing legal issues, Stride is involved in a security fraud class action lawsuit, investors allege that it misled the market about its performance, including claims of overstating student enrollment figure (ghost students) and not fully disclosing operational challenges. Additionally, there are complaints from a U.S school district accusing the company of regulatory violations and deceptive practices related to enrollment report as well as compliance. Although these claims have not all been proven in court such legal procedures can be costly as well as damages the company’s reputation and lead to financial penalties as well as operational restrictions which will negatively impact its revenues and long-term performance.

The company has faced repeated allegations regarding its enrollment practices and revenue recognition. In 2023 a whistleblower lawsuit claimed the company used a “fake internship program” to secure its funding’s of up to 300% per student (Fuzzy Panda Research, 2023). In 2025 Gallup-McKinley County schools accused the company of fraud and inflating enrollment through “Ghost students” (Glancy Law Firm,2025). This was followed by 2025-2026 investor class action lawsuits alleging the company is misleading disclosure that inflated the stock price before it fell by 50%. These issues build on earlier regulatory scrutiny and settlement of approximately of $168 million signaling ongoing risks.

Conclusion

Stride Inc stands as a high-quality digital education company with proven ability to scale its platform, generate strong and growing free cash as well as improve profitability. The company benefits from long-term contracted revenue, expanding demand for career focused education and a diversified presence across k-12 and adult learning markets. The company’s financial performance over the past 5 years indicate consistent execution with rising revenue, improving margin and strengthening cash generation all of which reinforce the durability of its business model.

Despite facing regulatory, legal risks and competition. The company’s fundamentals remain strong supported by accelerating growth. Based on DFCF model the stock appears significantly undervalued indicating the market is not fully pricing in its long-term earnings power as well as structural growth opportunities.

Disclaimer

The information provided by Moods Investment Research is for general informational and educational purposes only. It is not intended as, and does not constitute, financial, investment, tax, legal, or other advice. The content is not a solicitation or recommendation to buy, sell, or hold any securities or investment strategies.

All opinions expressed are based on current analysis and are subject to change without notice. While we strive for accuracy, Moods Investment Research

makes no representation or warranty as to the completeness, accuracy, or reliability of any information provided. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.

Moods Investment Research and its founders, directors, or affiliates are not liable for any losses or damages arising from any reliance on the information provided.

The views expressed in this article are those of the author(s) and do not constitute investment advice. The author does not hold a position in Stride (LRN) However, the author(s), including any editors or contributors (collectively referred to as “Moods and directors”), may or may not hold positions in other securities mentioned. Any such holdings are subject to change without notice.

Artificial intelligence (AI) technologies were used to support data processing, drafting, and/or analysis in this report. All conclusions and recommendations reflect the author’s independent judgment. While care has been taken to verify all information, neither the AI tools nor the authors guarantee accuracy or completeness. Therefore, whilst results derived from AI were reviewed for reliability; however, users should independently verify critical information.