Investment Thesis

Kraft Heinz (KHC) was merged in 2015 by Berkshire Hathaway and 3G Capital. The combined entity post-merger burdened the company with $30 billion in debt at the very beginning and that led to an aggressive cost cutting strategy for increased profitability. Besides strong brand presence, the company is struggling due to increased competition from Nestle, Unilever and Mondelez.

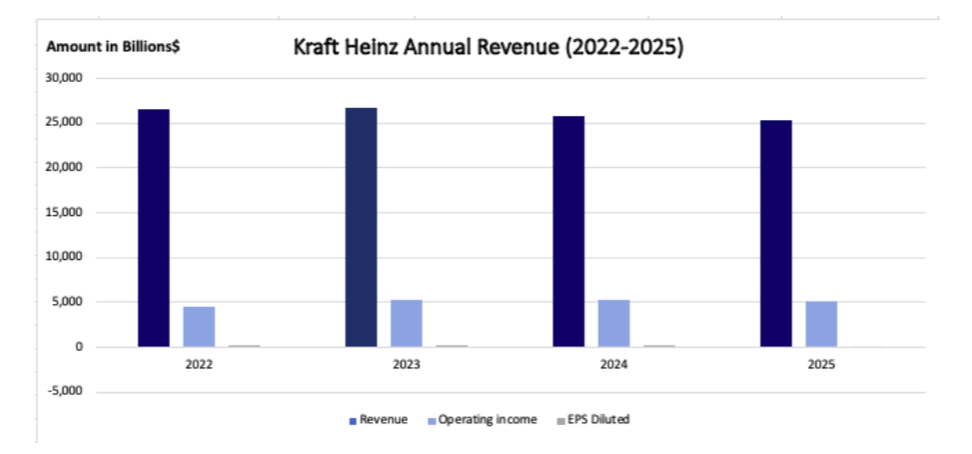

Between 2016 and 2024 the company reduced its debt by $10 billion after selling its natural cheese and nuts businesses. Despite financial distress due to competition and an impact during Covid-19 pandemic, the company still managed to produce surplus cash of approximately $3.2 billion in 2024 and paid more than 60% of that as dividends and the rest spent on share buybacks thus reflecting brand strength and sustainability of its business and its commitment to increase shareholder’s value. Despite these efforts the stock price remained depressed over the last one year losing its value by more than 30%.

Therefore, we believe the company has a lot of potential and based on our FCF valuation KHC seems to be significantly undervalued. Its stock price is expected to double in the next 4-5 years.

Company overview

Kraft was invented by James L. Kraft in 1903 in Illinois. In 1869 Henry John Heinz founded Heinz in Pennsylvania state. These two old companies were merged in 2015 by becoming Kraft Heinz Company (KHC) as a result of a partnership between Berkshire Hathaway and the Brazilian company 3G Capital increasing its market cap to $31- 32 billion. The company since then has always generated a sustainable free cash flow even during the economic volatility and uncertainty due to non-cyclical nature of the industry.

Kraft Heinz’s, Oscar Mayer and Planters products are globally recognized and enjoy higher consumer loyalty. Kraft Heinz as a global household name and a brand has customer stickiness. It is currently undergoing a strategic tax free spin off into Global Taste Elevation Co. and North American Grocery Co. which is expected to take effect in 2026 to enhance its value for its shareholders and consumers. It operates in over 40 countries with a strong presence in North America, Latin America and Europe.

Business Model and Competition

KHC has highly irreplaceable brands which are widely available all around the world with consistent quality at affordable prices. Its core revenue is driven by the sale of condiments, sauces, ready to eat meals and cheese which covers not only households but restaurants such as McDonald’s and other culinary institutions.

They are focused on healthier and plant based options to target more customers. KHC’s availability and accessibility makes it a strong cash generating business.

Their major retail and distribution partners are some of the biggest names like Costco, Carrefour, Kroger, Amazon, and Walmart. It also has a strong financial backing by a conglomerate like Berkshire Hathaway which makes the company more reputable and reliable when it comes to the quality of the brand and products .

Kraft Heinz’s revenue is contributed by six of its product categories to a large extent; which are Taste Elevation, Fast Fresh Meals, Easy Meals Made better, Real Food Snacking, Flavorful Hydration, and Easy Indulgent Desserts. The company heavily spends on R&D and has a team that is constantly working on diversifying its product range to cater to people from different countries with varying tastes and desires.

Kraft Heinz operates in Traditional Retail method and D2C Direct- to- Consumer business model. The products they manufacture are distributed through wholesale and retail to customers. And also, they advertise through website social platforms and delivering direct to its customers.

It is a brand selling the most demanded staple household food items. Their model rely on Consumer Packaged Goods (CPG) manufacturing for its efficient performance. People are not immune to popular brands like Philadelphia, Kraft Mac and Cheese, Heinz Ketchup, Capri Sun , Lunchables. With the strong marketing and R&D budget, their global reach is unimaginable.

On the other hand one of their competitors, Kirkland is a private label owned by Costco with lower per unit cost (20%) and huge supply deals. Although, Kirkland very quickly became famous for offering high quality products at unbeatable prices. In 2021, Kirkland brand contributed their share of 31% ($59 billion) to Costco’s total revenue.

Whereas, Kraft Heinz’s SG&A cost is relatively high per unit as compared to its competitor Kirkland. Kirkland is very aggressive with their supply deals and competitive prices because they spend less on marketing and stock keeping unit (SKU). KHC’s pricing strategy is a combination of value and cost effectiveness to counter increased competition and rising inflation. Kirkland on the other hand has a strategical arrangement with their suppliers that helps them achieve higher sales at a much lower cost and reduced prices without compromising on the quality for their products.

Therefore, in order to analyze its profit per SKU , KHC maintains SKU to keep a track on their inventory levels for their extensive products range. Whereas Kirkland prefers volume and membership than high gross margin per SKU.

Kraft Heinz is a globally recognized brand and their consumers pay premium for its quality and consistency. But in recent years the shift in demand due to affordability and often more options from the new low budget grocery brands such as Goodles’ Shella Good and Bling Bling Bac’n have started gaining strength and started dominating the consumer goods market.

Adding to their success story, Kirkland and Costco built up an excellent repertoire with the best in business brands for collaboration. For instance, Starbucks produces the House of Blends roasted coffee and also Kirkland batteries are made by Duracell thus ensuring their customers get high quality products at a much affordable prices.

On the other hand, if KHC has to compete it must improve its retail shelf space for more visibility and offer discounts to boost their sales to aggressively compete with the private labels such as Kirkland that is already offering irresistibly lower prices to Costco membership card holders.

Business Segments – Geographic

The company operates in three regional business segments geographically.

- North America which covers United States and Canada.

- International Development Markets (Europe and Pacific Developed Markets)

- Emerging Markets combines two segments; Western and Eastern Emerging Markets and Asia Emerging Markets

Source: Company’s 2024 annual report (10K)

Business Segments

Kraft Heinz’s Taste Elevation is the major contributor to its revenues contributing 44% whereas Easy Ready Meals contributes 18% of revenues.

Source: Company’s annual report (10K)

Despite having a strong brand name and undertaking a major cost cut KHC has not been able to increase its free cash flows, market value and its stock price since merger. Therefore, the company did not meet its shareholder’s expectations including that of 3G exiting their position last year in 2023 leaving Warren Buffett to remain one of its largest shareholder to this day.

There were other strategies tried by the company to reduce its debt by cutting dividends utilizing its surplus cash yet it did not materially improve its financial situation. For example, in the last 10 years the company’s dividend per share is reduced from $2.3 to $1.6 in 2025 (TTM).

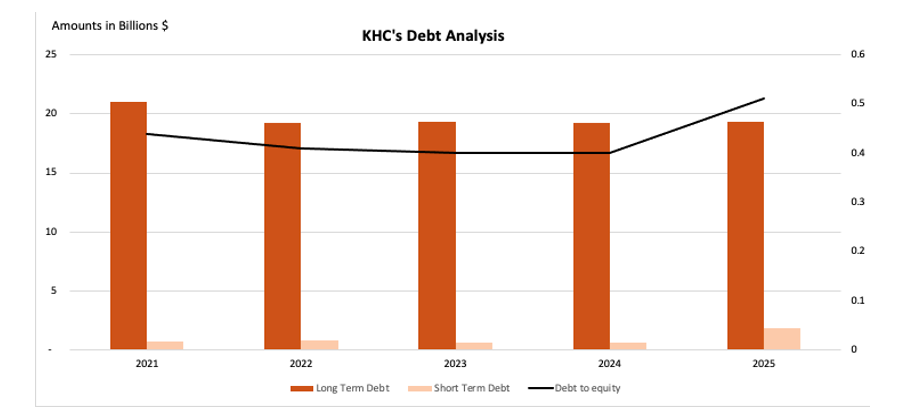

Therefore, KHC’s management is now more focused on selling off some of its assets. For example selling nut and cheese businesses in 2021 that helped reduce its debt from $25.15 billion to $19.22 billion in 2025.

In 2025, the company announced to sell its infant and specialty food business in Italy to NewPrinces S.p.A. which includes its subsidiaries, as part of its “NewPrinces Group. It includes brands like Plasmon, Nipiol, Dieterba and Aproten and Biaglut. They also sold their production facility in Italy which was being used for manufacturing some of these brands.

It is evident Kraft Heinz has changed its strategy to divesting from some of its low quality brands and businesses to improve its core business in order to strengthen its financial position and increase shareholder value.